Vision Vs. Execution

McDonald's Indian franchise Report Card!

Disclosure: Please note that these are my personal notes and not a recommendation to Buy, Hold or Sell. Do your own due diligence before initiating any position.

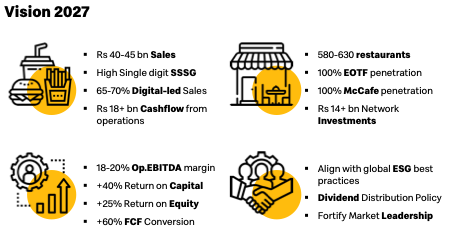

This is an extract of Westlife Foodworld (McDonalds master franchisee for South & West) Vision FY27 document which they had shared with the investors in end of 2022. Looks impressive!!!

While the presentation painted a picture of aggressive growth and financial efficiency, a closer look at historical performance and recent fiscal results reveals a significant disconnect between corporate aspirations and ground-level reality.

The primary challenge lies in the sheer scale of the jump required to meet these targets. To hit the sales goal from the FY23 baseline of INR 2,278 cr, the company needs a CAGR of 16.5%. Historically, however, Westlife has grown at a more modest 13% to 15% over the last 5 to 10 years. Difficult, but achievable!

The more optimistic part of the vision is the cash flow projection. Cumulative Cashflow from Operations (‘CFO’) for the last 5 years was INR 960 crs; company is aiming to achieve INR 1,800 crs (18 bln+) of cumulative CFO in the next 4 years as per its Vision Doc. This seems very difficult to achieve.

Company’s cumulative FCFF over the last 9 years was (-)ve INR 972 crs.

How would 60% of CFO start converting into FCFF is beyond comprehension, considering that average capex of additional restaurants is not going away.

“So overall, if you see on an annualized basis, we have already given the guidance that around INR200 crores to INR250 crores of the capex we are planning to incur versus 40 to 45 stores we are going to open, which will have a mix of drive-thru versus stand-alone versus mall store.” - Q2, FY24 Concall

To reach its goal of 600+ restaurants, Westlife must add approximately 263 new stores from its September FY23 baseline. At an estimated cost of INR 5 cr per restaurant, this requires a total outlay of roughly INR 1,315 cr. This heavy investment requirement makes the goal of high FCF conversion appear almost impossible to achieve.

Conclusion: One thing which clearly stands out - While it is nice to have a vision statement/document, company’s historical financial metric does not come close to what it wants to achieve.

Additional Info - The company has NOT earned ANY profit cumulatively over the last 10 years.

Far from accelerating toward its 2027 goals, recent performance shows a worrying downward trend:

Profit Erosion: After a net profit in FY23, earnings dipped 38% YoY in FY24 (INR 69 cr) and plummeted a further 82% YoY in FY25 to just INR 12 cr.

Stagnant Sales: Sales have remained largely range-bound between INR 2,278 - 2,491 cr.

Continued Negative Cash Flow: Cumulative FCFF for this period remained negative at -INR 267 cr.

While Westlife Foodworld’s Vision 2027 is impressive on paper, the company’s historical financial metrics and recent performance suggest a steep uphill battle. With zero cumulative profit earned over the last 10 years and dwindling margins in the short term, the gap between the "Vision" and "Execution" remains vast.

Ironically, Westlife is executing perfectly on one part of the plan: Store Expansion. They are opening 45-50 stores a year exactly as promised. However, this "blind execution" of expansion during a period of weak consumer demand is exactly what is crushing their margins and cash flow. It is a classic case of sticking to a growth map even when the terrain has changed.

After all, “Growth is always a component in the calculation of value... but not all growth is good.”