The Float Addiction

At what cost?

Disclosure: Please note that these are my personal notes and not a recommendation to Buy, Hold or Sell. Do your own due diligence before initiating any position. Also, I may have a position and hence may have biased views as well.

The other day, I came across Rahul, an underwriter friend of mine from one of the insurance companies. While we started chatting about a client, his first question was: What is the price (premium) the client is willing to pay? I was stumped by the question, I retorted:

Why don’t you underwrite the risk rather than price it?

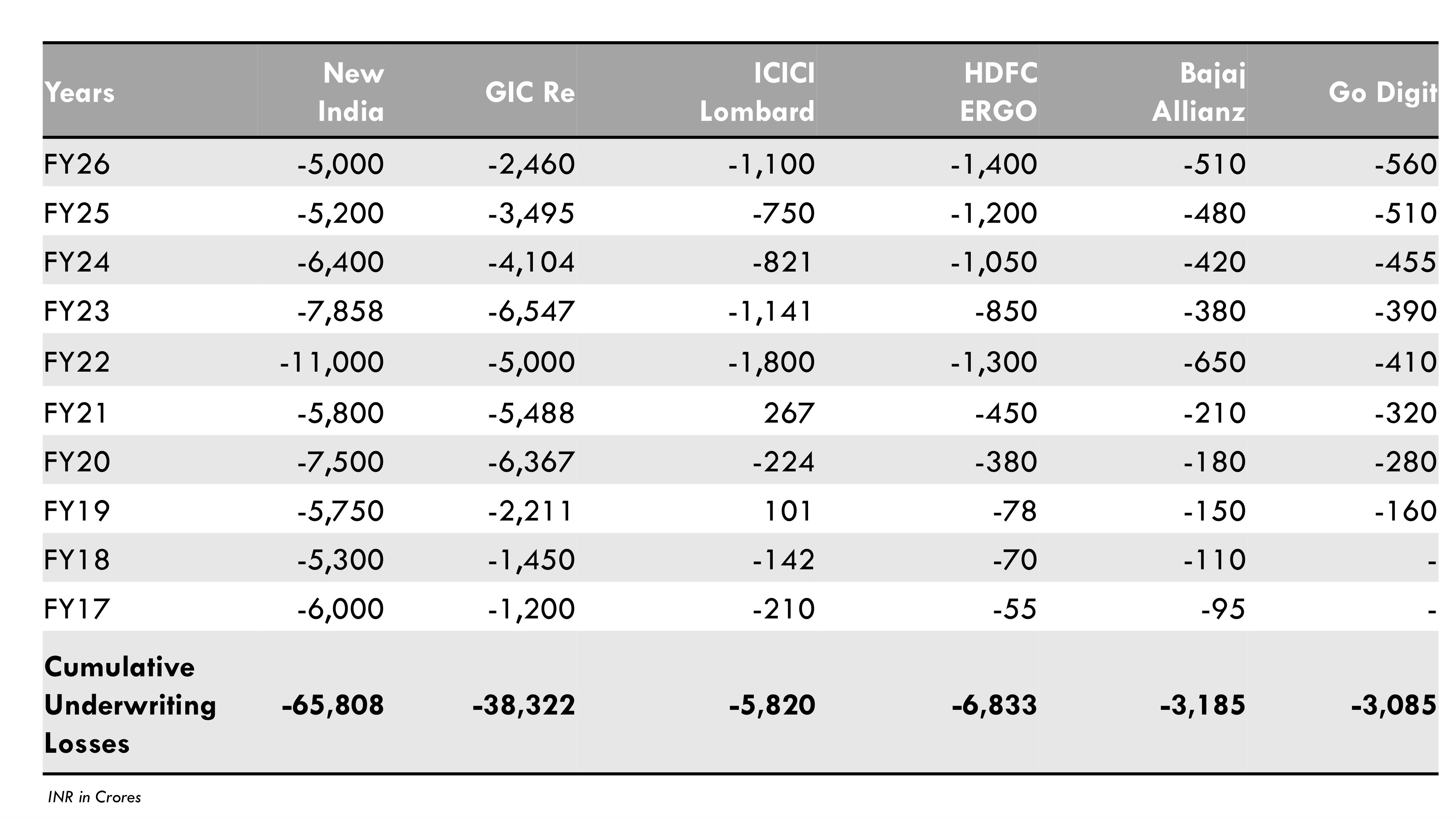

I later found out that most of the underwriters started with the same question in mind. Perhaps, that explained the underwriting losses of the insurance industry. The total underwriting losses of the Indian general insurers has been running negative for a long period of time. The below table shows that Indian insurers have incurred underwriting losses since a decade, every year, totalling to a cumulative ~INR 123,000 crores!!! (ICICI Lombard being an exception which had 2 years of underwriting profit in the last decade)

In the insurance world:

Underwriting Profit = Earned Premiums - (Incurred Losses + Underwriting Expenses)

While insurers talk about inadequate pricing, they however fail to walk the talk when it comes to underwriting principles. Below are some of my thoughts resulting in such outcomes:

Incentive caused bias: The yearly bonus of many CEOs of insurance companies is tied to the amount of business they generate, and not really based on how profitable the underwriting business has been. This is one of the primary reasons why they are keen to take up business, sometimes at any cost. Investment income supposedly, substitutes for the low/nil underwriting income.

Inability to sit calm: As Blaise Pascal had said “All of humanity’s problems stem from man’s inability to sit quietly in a room alone”. This is often the reason why insurers want to look busy rather than productive, often at the cost of doing unprofitable business.

Inability to sustain large performance variation: If the insurers were to voluntary let go businesses which are sub-optimally priced, it would be subject to large fluctuations in their volume of business. Valuations of businesses are often derived by increasing volume and pricing. While pricing in commodity-like industry, like insurance is often market determined where the insurance companies are mere price takers, volume is the only way wherein increased revenues can be generated, often providing an illusion of enhanced value creation.

Low barriers to entry: With no major losses having been witnessed in the last couple of years in the insurance industry, capital availability is not a challenge, thereby insurers wanting to deploy cheap (mostly) capital by underwriting businesses, often with an intention of generating float/investment income alone. It is only through their investment income that some of them have shown net profits over the years.

Information overload Fallacy: Since some of the insurers have been underwriting the same risk since many years in a row, they perceive that they know the account “inside-out”, thereby failing to see obvious or emerging risks. Cyber was an implied risk some years back which was not being priced in the premiums, despite the existence of that risk. Often, the businesses are underwritten basis relationship rather than from a risk perspective.

Sunk Cost Fallacy: Cumulative prior investment of time and effort often makes the insurers susceptible to sunk cost fallacy, wherein they want to continue their decision of underwriting even if the expected underwriting loss outweighs the expected float income. It’s like sitting through a crap movie just because you have spent money on it.

Everyone else is doing it/Envy Bias: This is one of the cardinal sins of insurance business. It takes huge underwriting discipline to select the businesses an underwriter would be keen to look at “independently”. Just because your neighbor is getting richer faster than you, you start to get envious; that’s foolishness.

While, Rahul did win the business of the client in question, it led me to wonder, at what cost?